Investing for the Long-term

- Purchase securities with a view to holding for the long term with annual portfolio turnover averaging roughly 25% or less. Furthermore, low portfolio turnover minimizes transaction costs and taxes (when applicable), thereby increasing portfolio investment returns.

- Additionally, a focus on the long-term does not create the compulsion to “do something” in periods of short-term volatility (other than look for exceptional buying opportunities).

Dilution from Owning Mediocre Stocks

Owning additional securities in a portfolio solely for the sake of diversification is short-sighted, at best . Furthermore, making purchases of this nature typically increases the risk of a poor investment decision thereby mitigating, at least partially, the benefits of owning a portfolio of truly exceptional companies. Failing to adhere to a proven investment process – and buying securities that do not withstand the scrutiny of that process – is an almost certain recipe for mediocre investment returns at best and more likely a significant loss of capital.

. Furthermore, making purchases of this nature typically increases the risk of a poor investment decision thereby mitigating, at least partially, the benefits of owning a portfolio of truly exceptional companies. Failing to adhere to a proven investment process – and buying securities that do not withstand the scrutiny of that process – is an almost certain recipe for mediocre investment returns at best and more likely a significant loss of capital.

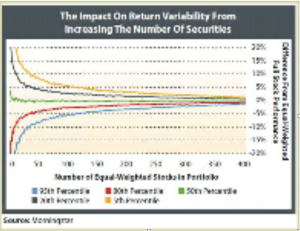

Additionally, there are numerous studies from the academic community and practitioner’s alike that refute the notion one must own 75 securities (or the mutual fund average of 172 holdings) to be adequately diversified

Perhaps Warren Buffett explained it best: “Wide diversification is only required when investors do not understand what they are doing.”

Through extensive and time-intensive investment research and analysis combined with CastlePoint’s intense focus on security selection results in a portfolio of about 30 stocks.

A fund’s investment returns cannot surpass the benchmark if it highly resembles or owns a vast majority of the securities in the index. As such, independent research and analysis is at the core of each investment decision at CastlePoint: thoroughly understanding the reasons for buying and continuing to own a stock provides the insight necessary for understanding when to sell it.

The presence or absence of a company presence in an index is irrelevant in CastlePoint’s decision-making process, which general results in portfolios with a tracking error about 3% to 5%

Nevertheless. the core investment approach and philosophy remain unchanged. The firm manages investment portfolios from two satellite offices, one in the San Francisco Bay Area and the other in Atlanta, GA. CastlePoint, with fewer than $10 million in assets, is an independent advisor currently exempt from SEC and State regulatory reporting requirements

Nevertheless. the core investment approach and philosophy remain unchanged. The firm manages investment portfolios from two satellite offices, one in the San Francisco Bay Area and the other in Atlanta, GA. CastlePoint, with fewer than $10 million in assets, is an independent advisor currently exempt from SEC and State regulatory reporting requirements{kind=link}

{kind=link}