CastlePoint’s enviable risk-adjusted investment returns stem from a disciplined, analytically rigorous process based on proprietary research, artfully implemented financial theory, and decades of investment experience.

CastlePoint Investment Group, LLC, is an independent investment advisory firm that specializes in creating wealth for clients by actively managing focused, large cap equity portfolios for institutions as well as high net worth individuals.

CastlePoint’s enviable risk-adjusted investment returns stem from a disciplined, analytically rigorous process based on proprietary research, artfully implemented financial theory, and decades of investment experience.

It’s virtually impossible to thoroughly research and analyze a portfolio of 172 securities – the average number held by the typical large cap equity mutual fund according to Morningstar – and consistently apply the same high standards to each investment decision. CastlePoint takes a different approach.

The firm’s investment philosophy is based on thoroughly researched and widely accepted financial concepts thoughtfully chosen and uniquely woven together. The end result is a well crafted, time tested process that systematically exploits enduring market anomalies (refer to PDF file on right for further details).

CastlePoint maintains long-term investment success is the reward earned for consistently applying a clearly-defined, thoughtfully-constructed, and intellectually-honest investment process and, importantly, adhering to that process when the pressure to abandon it is greatest.

CastlePoint’s partners invest their equity portfolios in one or more of the firm’s products – so we, and our families, “eat what we cook.”

This vividly illustrates our confidence in the intellectual honesty and integrity of CastlePoint’s investment process. It shows a steadfast belief in the significant long-term capital appreciation potential for securities in client portfolios and an unambiguous incentive for us to produce exceptional, risk-adjusted investment returns.

As such, CastlePoint limits portfolio holdings to a more manageable level of about 30 securities. This allows us to conduct thorough due diligence and scrutinize each investment while also offering sufficient portfolio diversification.

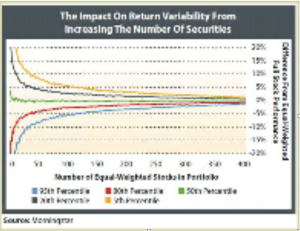

As shown in the chart below, the largest decrease in portfolio risk occurs where the lines are steepest. Once this inflection point is passed and the curves flatten, the incremental benefit of adding more stocks to the portfolio increase, but at a significantly declining rate.

Owning additional securities in a portfolio solely for the sake of diversification is short-sighted, at best . Furthermore, making purchases of this nature typically increases the risk of a poor investment decision thereby mitigating, at least partially, the benefits of owning a portfolio of truly exceptional companies. Failing to adhere to a proven investment process – and buying securities that do not withstand the scrutiny of that process – is an almost certain recipe for mediocre investment returns at best and more likely a significant loss of capital.

. Furthermore, making purchases of this nature typically increases the risk of a poor investment decision thereby mitigating, at least partially, the benefits of owning a portfolio of truly exceptional companies. Failing to adhere to a proven investment process – and buying securities that do not withstand the scrutiny of that process – is an almost certain recipe for mediocre investment returns at best and more likely a significant loss of capital.

Additionally, there are numerous studies from the academic community and practitioner’s alike that refute the notion one must own 75 securities (or the mutual fund average of 172 holdings) to be adequately diversified

Perhaps Warren Buffett explained it best: “Wide diversification is only required when investors do not understand what they are doing.”

Through extensive and time-intensive investment research and analysis combined with CastlePoint’s intense focus on security selection results in a portfolio of about 30 stocks.

A fund’s investment returns cannot surpass the benchmark if it highly resembles or owns a vast majority of the securities in the index. As such, independent research and analysis is at the core of each investment decision at CastlePoint: thoroughly understanding the reasons for buying and continuing to own a stock provides the insight necessary for understanding when to sell it.

The presence or absence of a company presence in an index is irrelevant in CastlePoint’s decision-making process, which general results in portfolios with a tracking error about 3% to 5%

CastlePoint’s investment philosophy is based on investors’ tendency to commit cognitive such as Representativeness, Availability, and Anchoring as defined below. These mistakes cause the market price of a company to fluctuate far more widely than its underlying fundamentals, which tend to change gradually over time.

Behavioral finance is the study of how the psychology of investors’ behavior and the subsequent impact on the market. In addition to the overreaction hypothesis, it includes how people make judgments under uncertainty. For example:

Behavioral finance is the study of how the psychology of investors’ behavior and the subsequent impact on the market. In addition to the overreaction hypothesis, it includes how people make judgments under uncertainty. For example:

CastlePoint successfully employs the same time-tested investment approach used for over two decades creating portfolio that outperform the index with less than market risk with relatively high consistency. Over the years after extensive empirical research and analysis, several elements of the investment model used to screen prospective additions were meticulously reevaluated and fine-tuned to insure continued excellent results.  Nevertheless. the core investment approach and philosophy remain unchanged. The firm manages investment portfolios from two satellite offices, one in the San Francisco Bay Area and the other in Atlanta, GA. CastlePoint, with fewer than $10 million in assets, is an independent advisor currently exempt from SEC and State regulatory reporting requirements

Nevertheless. the core investment approach and philosophy remain unchanged. The firm manages investment portfolios from two satellite offices, one in the San Francisco Bay Area and the other in Atlanta, GA. CastlePoint, with fewer than $10 million in assets, is an independent advisor currently exempt from SEC and State regulatory reporting requirements